The global financial ecosystem is built on accounts. Users have billions of accounts with financial institutions to manage their assets, currencies, and all other financial instruments – hundreds of trillions of dollars in total account value. Transacting between these accounts is what makes up our financial ecosystem – paying, investing, trading, transferring, lending, borrowing, and so on.

If we look under the hood, it is a 50-year-old spaghetti of incompatible accounts, trying to trade across thousands of financial institutions, manual processes, different systems and networks, competing infrastructure providers, various asset classes, currencies, and jurisdictions. Most of these platforms were designed not only before the digital age, but also before the mobile or even the internet age. And

talking about age, SWIFT, one of the major financial infrastructure pieces, is 48 years old, FIX is 30 years old, and VISA is 63.

As we have seen in every other information based industry, digital transformation is not about “fixing” old systems – it is a switch to a new paradigm which changes everything. Netflix didn’t fix cinema and television – it offered the market a new paradigm, which incumbents had to copy.

The unified theory of digital financial markets: Every account will become a digital wallet

How is a digital wallet different from a traditional financial account?

- It has a global address (much like an internet IP) which ledgers can assign value to

- It has a private key letting users and custodians sign transactions to prove intent

- It allows direct and instant trading between wallets

Therefore, when all accounts are digital – all transactions can be direct and instant, making everything in the middle redundant. Turning accounts into digital wallets will remove massive layers of intermediary complexity, manual processes, reconciliations, margins, delays, errors, risks, and costs. This financial digital transformation is also driven by another unique capability of digital infrastructure: wallets can interact with smart contracts, enabling automated execution of agreements.

With instant, direct transactions, and agreement automation, the real impact of this digital

transformation goes well beyond optimization and cost cutting. Digital wallets enable new services and business models that will completely change the dynamics of entire markets.

Lastly, and perhaps most importantly, the unified theory of digital financial markets has a key advantage: it can be deployed gradually.

Digital wallet-based services will be deployed over time in every financial submarket. Once they are deployed in a particular submarket, competitors in the space will be compelled to follow suit, given the better products, services, cost structure, distribution, liquidity, and business models enabled by digitization.

The implication of digitization for financial institutions

Digitization, enabling direct transactions between users and assets, does not spell doom for financial

institutions. Rather, this is an opportunity not only for digital-native newcomers but also for the incumbents with their resources, reach, and regulatory coverage – provided that they can see the strategic tectonic shift and mobilize their troops.

The vast majority of digital wallets are and will continue to be managed professionally for users by financial institutions, and in the traditional financial markets, exclusively by regulated financial institutions. However, it is important for financial institutions to read the map of the new digital battleground, which will be decided on three main fronts:

- Who can digitize the best assets and offerings and bring them online

- Who can deploy secure digital wallet-based accounts with the best clients?

- Who can best utilize distribution, technology, and data to connect the two?

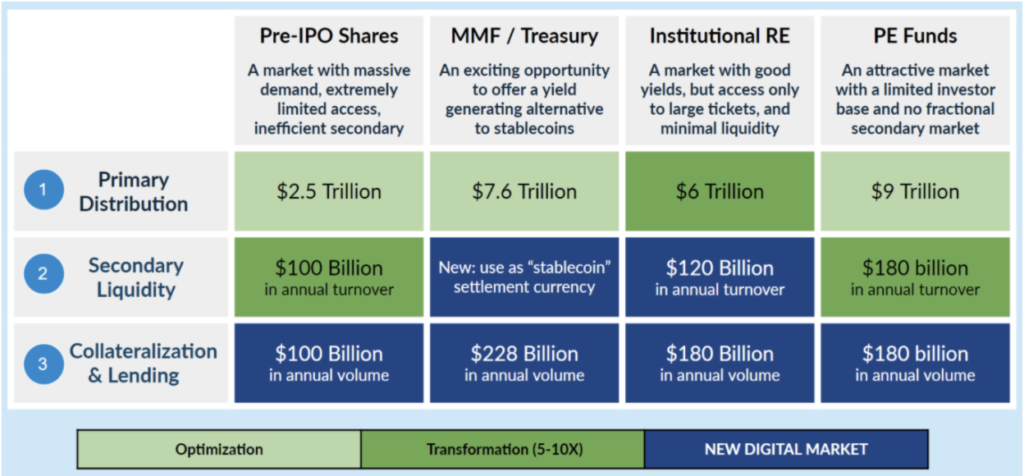

Starting with private markets

Digital financial technology was born in the crypto space, and therefore the market assumed that the first

implementation of digital wallets in financial institutions will be around crypto.

Crypto is still a regulatory landmine for financial institutions and most have not yet deployed it. I believe they will, but it really depends more on regulators than the financial institutions themselves. Regulators are not paid to be early adopters.

Instead, the majority of financial institutions are deploying digital securities first. Yet, with smart planning, those same wallets deployed today with the best clients will tomorrow be used to trade any digital asset – from digitally-native assets, to public assets, derivatives, and any other asset class.

Years ago, when the world’s communication market switched from landline to mobile, some markets didn’t have landlines. Countries jumped straight to mobile. The same thing is happening now in the private markets.

Unlike public markets, which are already automated, private markets are stuck in the manual phase. There is almost no technology infrastructure, no “spaghetti” to replace. This makes private markets ideal for the deployment of the new digital solutions. When you can turn a manual investment process that takes two months into a one-second click, you clearly have a winner.

Not only that, private markets are growing at an unrepentant rate. In September 2021, Blackrock said, that “we believe that the allocation to private markets in wealth portfolios should increase from 5% today

to 20%.”

In addition, in private markets, digital ledgers are replacing Excel sheets and papers. When it comes to existing regulation, digitization clearly delivers better services and transparency.

The GDF Private Market Digitization Steering Group

Over the last year and a half, a group of some 70 major banks, asset managers, exchanges, fintechs, and legal experts have been working together under the leadership of GDF, to develop an open source protocol to interconnect all the various components of the new digital private markets. The protocol is called FinP2P.

FinP2P is not a blockchain in itself, it is a routing network, a trading pipeline, allowing financial institutions to connect assets from any source, and on the other side give clients a digital wallet that connects them to all suitable assets, as well as other wallets. The protocol then acts as a pipeline that allows everyone to trade with everyone (within regulation and permissions) – thereby enabling the core promises of the unified theory of digital financial markets.

Conclusion

Financial accounts will become digital over time and enable direct and instant transactions between wallets and assets. This vision is materializing in front of our eyes as financial institutions all over the world are starting to digitize assets, deploy digital wallets, and the FinP2P pipeline will connect them all.

While these digital wallets will initially be deployed for private-market applications, they will in time support crypto assets, public equities, derivatives, and any other financial asset. The race to digital market leadership is on.