The shear idiocy of human beings is in danger of losing its capacity to shock. Faced with an existential threat to their continued species survival, rather than pouring all their efforts into attempts to reverse or even halt anthropogenic climate change, some still cling to magical thinking and hope we can persevere with inherited models of production and consumption as we coast toward disaster.

Cryptoassets, whether intangible coins or pictures of cats, now generate more than 90.2 million metric tons of CO2 per year and consume more energy than small nations such as Malaysia or Sweden (around 110TWh per year). That said, the industry and policy makers are addressing this issue. Countries such as China are beginning to push regulation of mining, causing seismic readjustment in the value of Bitcoin. In response some platforms, such as Ethereum (which is the basis for most NFTs), have plans to transition to a proof of stake system which will reduce the energy consumption of Ethereum-based cryptos and blockchains by an estimated 99.5%.

However, tempting as it is to roll one’s eyes at the perceived folly of people willing to speculatively trade Bitcoin, it is important not to lump all of fintech into this category.

Fintech – “the integration of technology into offerings by financial services companies in order to improve their use and delivery to consumers” (Investopedia) – offers a host of benefits to sustainability and the fight against climate change.

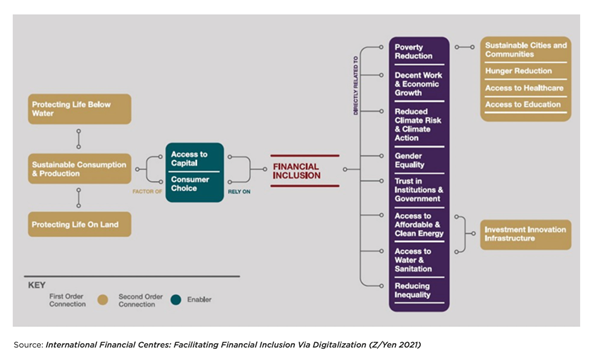

Financial inclusion – banking the unbanked (through smartphone networks), giving official identity (and agency) to the billions who have none, providing insurance for farmers in developing nations and crowdsourcing finance for small businesses – is just one area that has caught the attention of forward thinking international financial centres. An excellent example can be found in Labuan IFBC in Malaysia, which is assessing how fintech enabled financial inclusion can be used to deliver the UN Sustainable Development Goals.

Smart contracts are another technology delivering the (green) goods – from simplifying the contracts for green bonds, to providing supporting infrastructure on green loans and providing chain of custody and provenance for responsible supply chains. Distributed ledgers, with their ability to validate, record, and track transactions across a network of decentralized computer systems, are revolutionizing the banking and insurance sectors, and allowing the creation of a host of new products and services that can support the transition of a low carbon economy.

‘Digital fairy dust’ is not a universal panacea. Significant challenges remain if we are to use fintech to restructure our financial systems to provide support in our fight for biodiversity, social justice, and climate change. Goodness knows it needs it: COVID-19 dealt a hammer blow to the world economy, setting back progress on the Sustainable Development Goals by years. Fintech offers a host of benefits which could enable low-carbon green growth, enabling developing economies to bridge this gap and deliver stable, equitable growth for their citizens.

However, though the rise of fintech may mean that the physical constraints of infrastructure and systems have been removed as an obstacle to trade, significant legislative and policy barriers remain and are likely to increase.

Conflation of fintech with cryptocurrency’s public image is not helpful. Development economics and financial technology are complex topics. Many policy makers are ill-versed in the fundamentals of financial services and easily swayed by public opinion.

The merging of fintech and green finance represents an enormous opportunity to square the circle in the creation of lucrative new markets and the delivery of public goods. However, to unlock this potential, policy makers and the public must be brought on side. To address this, financial centres should work together to frame the right questions for policy makers, regulators and financial service providers on the implications of embedding fintech into financial systems and how this can deliver on sustainability, ESG, and climate action.

Read more from the report, Digital Assets: Laying ESG Foundations